New $14-Million Recovery Center Is Launched

A 52-unit, $14-million version of the innovative Fletcher Group model of recovery housing will soon be a reality, thanks to the hard work of numerous partners devoted to helping people recover from drug addiction.

Ground for the new 52-unit Cumberland River RHOAR (Recovery, Hope, Opportunity, and Resiliency) Center, was broken on October 12 in Middlesboro, Kentucky. Scheduled to open in late 2023 or early 2024, the facility will give women beset by addiction in Bell County a safe place in which to live, recover, grow and reunite with loved ones.

The ground-breaking ceremony was extensively covered by local media (see links below) and attended by numerous dignitaries including U.S. Representative Hal Rogers, Kentucky Lieutenant Governor Jacqueline Coleman and former Kentucky Governor Dr. Ernie Fletcher, founder and Chief Medical Officer of the Fletcher Group.

When finished, the RHOAR Center will accommodate 112 women in 30 single-bed rooms and 12 two-bed rooms, ten efficiency units and 18 shelter beds. In accordance with the highly successful Recovery Kentucky model that Dr. Fletcher pioneered when governor of Kentucky, the center will provide the full continuum of care—including drug withdrawal support, counseling, education and employment—to facilitate lasting abstinence and recovery.

“We’re coming up on the jackpot,” said Rogers after recounting the years-long journey to fully fund the center. “An actual physical place where we can administer treatment for people with addiction who can’t help themselves. This is the best example of being your brother’s and sister’s keeper that I can think of.”

“There is not a family in Kentucky that hasn’t felt that pain,” said Lieutenant Governor Jacqueline Coleman . “I’m just so grateful that we are here today to celebrate something that is going to make a difference not just in one person’s life but in the future and the trajectory of their family’s life. That is absolutely game-changing.”

This project grew out of the Fletcher Group’s RHOAR initiative, which was funded in part by the Appalachian Regional Commission to assist the hardest-hit coal economies of eastern Kentucky. Funding for the $14-million project came from several sources, including the Kentucky Housing Corporation, which will provide over $900,000 in Low-Income Housing Tax Credits in each of the next ten years as well as $4 million from the Federal Housing Trust Fund. The Federal Home Loan Bank of Cincinnati, Ohio Capital Corporation for Housing and Bell County Economic Development also provided significant development funds for the project. The RHOAR Center will be developed and operated by Cumberland River Behavioral Health, a non-profit community health center serving eight southeastern Kentucky counties.

Watch the Video!

To watch a video about the grand opening of the new Cumberland River RHOAR Center for Women in Middlesboro, Kentucky on May 16, 2024, simply click the image on the left.

Valuable Links

- News Coverage

- Lane Report article covering the ceremony

- Video of the Ground-Breaking Ceremony

- How Low-Income Housing Tax Credits Work and Who They Serve

How Low-Income Housing Tax Credits Work

The Low-Income Housing Tax Credit (often referred to as “LIHTC”) originated as part of the United States’ 1986 Tax Reform Act. LIHTC supports affordable rental housing by subsidizing acquisition, construction, and rehabilitation of units for low and moderate income tenants. More than 3 million units of affordable housing have been assisted with LIHTC, making it the nation’s largest source financing for affordable housing.

How it works

The Internal Revenue Service allocates Low-Income Housing Tax Credits to the states’ Housing Finance Authorities (HFA). The HFAs award the credits on a competitive basis to affordable housing developers (including nonprofit developers) who sell the credits to investors who purchase them to offset taxes over the next ten years. The award of the credits to developers is made through a process defined in each state’s Qualified Assistance Plan (QAP). HFAs must comply with the Department of Housing and Urban Development’s (HUD) affordability standards but can include additional requirements.

The amount of available LIHTC changes annually. In 2022, $870M of credits were available for the entire nation. LIHTC is allocated based on the greater of $2.60 per state population or $2,975,000 – whichever is larger. The “multiplier” (currently $2.60 per person) is also subject to annual changes.

How to qualify

Recovery Houses that propose to serve low-income populations may qualify for LIHTC through one of the following ways:

- At least 20% of the project’s housing units will be occupied by tenants whose incomes are 50% or less of area median income (AMI).

- At least 40% of the housing units will be occupied by tenants whose incomes are 60% or less of AMI.

- At least 40% of the housing units will be occupied by tenants whose incomes average 60% or less of AMI, with no units being occupied by tenants with incomes that exceed 80% of AMI.

In all cases, rents cannot exceed 30% of income. It is allowable for a LIHTC developer to restrict up to 100% of units to tenants with qualifying incomes. This is to the advantage of the project since credits are awarded only for the portion of the building that is occupied by low-income tenants. The project must comply with income levels and rent limitations for at least 15 years. In addition there may be an additional 15 years of compliance required as stipulated in an “extended use agreement”.

Developers (or their syndicators) sell the tax credits to an investor. The money from this sale allows the developer to receive equity (funds) to complete the affordable housing project. Since most of the equity from the sale of the credits isn’t paid until the project is fully occupied, interim financing (such as a construction loan) if often needed. LIHTC will not provide enough equity to finance the entire project. In Additional funding (for example, grants such as the Community Development Block Grant) will have to be secured for a debt free project. Smaller projects (such as those with fewer than 30 units of housing may not be competitive for LIHTC). Securing guaranteed rental income, for example Section 8 Project Based Housing Vouchers, contributes to the ongoing operating costs of the housing program.

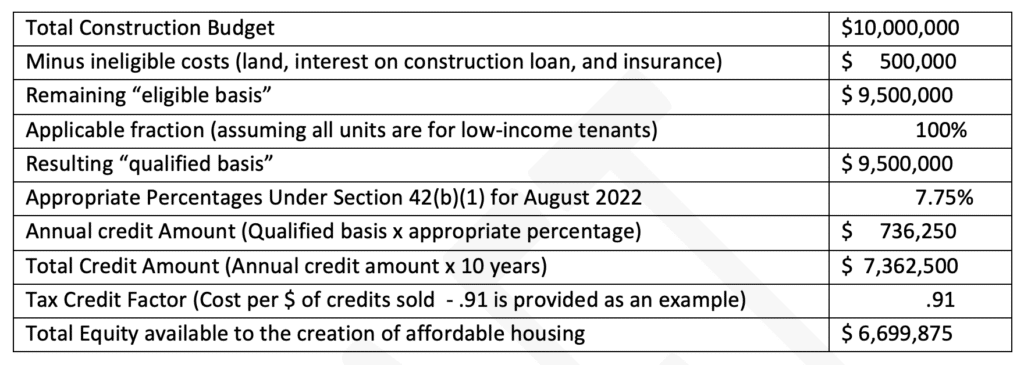

In the above example approx. 67% of the project is financed by LIHTC. If this project was located in a Qualified Census Tract (QCT), it could qualify for a High Cost Adjustment Boost (additional 30%) and LIHTC could cover 87% ($8,709,837) of the project (if credits were sold at .91).

A partnership structure such as a Limited Liability Corporation or Limited Liability Limited Partnership is formed between the Limited Partner (the Investor) and the non-profit organization (the General Partner). The General Partner manages the day-to-day operations of the partnership and the Limited Partner’s primary role is to provide an investment to the project and control terms of the partnership agreement. Participating in such a structure presents both benefits and risks to the non-profit General Partner.

The Benefits

- Substantial amount of equity available for project development. Without this funding the non-profit may not otherwise be able to develop affordable housing units.

- The non-profit stands to be paid developer fees, property management and/or other fees

- Opportunity to own the project at the end of the 15 year compliance period

The Risks

- Market conditions can influence the pricing that is paid to the non-profit for the credits

- Changes in economic conditions could impact financial viability and lead to lost credits

- Uncontrollable delays in opening the project as projected could result in the loss of credits

- Credits could also be lost or recaptured if the rate of low-income tenancy changes

As both the benefits and risks of participating in a LIHTC partnership are significant for the General Partner, it’s essential that non-profit organizations serving in this role rely on the guidance of experienced attorneys and LIHTC consultants to minimize risks and protect interests.

This web page is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health and Human Services (HHS) as part of an award totaling $17.1 million with 0% financed with non-governmental sources. The contents are those of the author(s) and do not necessarily represent the official views of, nor an endorsement, by HRSA, HHS, or the U.S. Government.